Bank Redirects Are a Popular Form of Online Transaction; Here’s When to Use Them

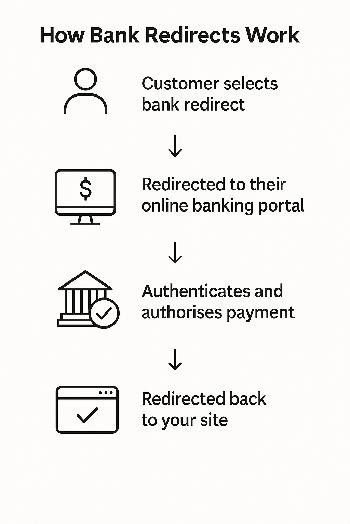

Bank redirect payments allow customers to complete purchases by logging into their online banking portal, authorising the payment, then returning to your site. This method offers a secure, familiar experience for shoppers and supports fast, verified transactions without card details.

They offer strong security through direct bank verification, higher conversion rates where customers favour bank transfers, and faster processing. Customers keep their banking details private and card data never passes through your systems.

Benefits of Bank Redirect Payments and When to Use Them

Bank redirect payments allow customers to pay directly from their bank accounts by redirecting them to their bank’s secure online portal for authentication and approval. This method, often called “pay by bank,” is widely used in markets such as the UK, the Netherlands, Spain, Finland and Germany.

The primary benefit is security. Customers authenticate payments through their bank’s interface, which typically includes strong authentication measures like two-factor verification. Because sensitive banking data never passes through your systems, the risk of fraud is lower than with card transactions.

Bank redirect payments also deliver higher conversion rates in markets where consumers prefer bank transfers. For example, Bancontact is popular in Belgium and FPX is widely used in Malaysia.

This payment method is particularly effective for retail businesses expanding into Europe and Asia Pacific, where offering locally preferred options drives sales. B2B companies can also benefit, as bank-to-bank transfers align with the professional expectations of corporate payments and are ideal for high-value transactions. In countries with low credit card penetration, bank redirects open access to customers unable to use cards.

There are limitations. Some bank redirect methods do not support recurring payments, so they are less suitable for subscription models. Additionally, because customers are temporarily redirected away from your site to complete payment, the process can introduce friction and increase the chance of drop-off.

How to Configure Bank Redirect Payments Across Different Markets

Europe

Europe leads global bank redirect usage, with these methods accounting for over half of online commerce in countries such as Germany.

Payment methods by country:

- Germany: Sofort

- Belgium: Bancontact

- Austria: EPS

- Poland: P24 and BLIK

- Switzerland: TWINT

Configuration requirements include:

- Compliance with Strong Customer Authentication (SCA) under PSD2 regulations

- Support for two-factor authentication flows, which may extend processing times

- Settlement typically within 1–2 business days, varying by country

- Primary currency support in euros (EUR)

- Inclusion of currency and country parameters in payment requests

Asia Pacific

Bank redirect payments are widely used across the Asia Pacific region, where consumers favour direct bank transfers for online purchases. Malaysia is a strong example, with FPX supporting a large share of transactions. Other markets in the region also offer local redirect schemes that cater to similar preferences.

Regional considerations:

- High mobile usage demands mobile-optimised redirect flows

- Bank transfers help address lower credit card penetration, supporting financial inclusion

- Settlement times vary significantly across countries

- Multi-currency handling is often required, calling for a payment solution with built-in FX

Americas and Other Regions

Bank redirect adoption remains limited but is growing, particularly for B2B transactions. Digital redirect capabilities are developing as regional banks digitise.

Market characteristics include:

- North America focuses mainly on B2B payments rather than consumer use

- Digital adoption varies between urban and rural customers

- Latin America is experiencing rapid growth in smartphone-based payments

- Regulatory frameworks differ widely across countries

Configuration priorities:

- Strong fallback payment options are necessary due to variable infrastructure

- Settlement times tend to be longer

- Multi-currency support is commonly needed

- Compliance with diverse local regulations is essential

How Bank Redirect Payments Improve Security and Simplify Compliance

Bank redirect payments enhance security by ensuring sensitive banking credentials never pass through merchant systems. Customers authenticate directly with their bank, reducing the risk of data breaches and fraud. This direct bank authentication creates a secure connection between customer and bank, eliminating the need for merchants to store or transmit financial data.

Most bank redirect methods incorporate two-factor authentication, such as SMS codes or mobile app verification, adding an extra layer of protection. This reduces fraudulent transactions compared to typical card-not-present scenarios.

Bank redirect payments also simplify compliance with regulations like the European Union’s PSD2 and Strong Customer Authentication (SCA) requirements. Because authentication occurs through the bank’s systems, businesses avoid much of the burden associated with meeting these standards.

Beyond Europe, as open banking expands worldwide, bank redirect payments position businesses to meet evolving regulatory demands while maintaining consistent security levels across markets.

Additionally, these payments reduce merchants’ PCI compliance scope since card data never touches their infrastructure, lowering operational costs and liability. By shifting authentication and fraud prevention to trusted banks, bank redirects reduce merchant risk and support a more secure, compliant payment ecosystem that can scale as security standards evolve.

Bank Redirect Payments Versus Cards and Digital Wallets

Your payment method choice directly impacts conversion rates and costs. This framework shows exactly when bank redirect payments outperform other options.

| Factor | Bank Redirect Payments | Credit/Debit Cards | Digital Wallets |

| —– | —– | —– | —– |

| Transaction Cost | More economical | Higher processing costs | Variable |

| Fraud Risk | Low (direct bank auth) | Medium (card-not-present) | Medium |

| Settlement Speed | Variable by region | 1-3 business days | Often faster |

| User Familiarity | High in specific regions | Universal | Growing rapidly |

| Recurring Payments | Limited support | Strong support | Good support |

| Refund Process | Sometimes limited | Well-established | Well-established |

| Global Coverage | Regional strength | Near-universal | Growing |

Offer Bank Redirect Payments in Key Markets

Position bank redirects as a secondary option, along with other alternative payment methods, when accepting card payments. This approach respects local preferences while maintaining card payments for most customers.

Consider Your Business Model

Bank redirect payments perform well for retail businesses targeting Europe and Asia Pacific, especially for higher-value purchases where security takes priority over convenience.

Subscription models require caution, as bank redirects often lack reliable recurring payment support. B2B companies benefit from bank redirects for one-off payments, as business customers commonly favour bank transfers for larger transactions over cards.

Avoid Choosing Either-Or

Rapyd Collect allows simultaneous integration of multiple payment methods. Implement intelligent payment selection that presents the most relevant options based on factors like customer location, transaction size and payment history.

This strategy future-proofs your payment infrastructure while maximising conversion across diverse markets. Offering customers a choice while guiding them to the most effective payment method is integral to smart payment optimisation.

Get Started with Bank Redirect Payments Today

Choosing the right payment methods, including bank redirect payments, is essential for expanding your business globally and maximising conversions. Whether you accept payments from one country or worldwide, Rapyd Collect simplifies the process. With direct card acquiring and support for hundreds of local payment methods, your checkout flows smoothly and more revenue flows to you.

Contact Rapyd to learn how to optimise payments for your business.

Subscribe Via Email

Thank You!

You’ve Been Subscribed.